Open Letter to EU on Open Banking

Who needs to benefit from it? Only banks and companies?

(the following text is my own, partial translation and adaptation of an open letter by Giovanni Biscuolo, sent on December 16th, 2019 to the Nexa mailing list, with CC-BY-SA 4.0 license, and published with the same license)

Dear EU, I knew little or nothing about your Payment Services Directive, version 2 (PSD2), but I decided to learn more when I came across an italian article titled [“Open banking, a little-known revolution is underway. And everything will be in the hands of customers”] (https://www.ilfattoquotidiano.it/2019/12/14/open-banking-e-in-corso-una-rivoluzione-di-cui-pochi-parlano-e-tutto-sara-nelle-mani-dei-clienti/5612425/).

“All in the hands of the customers”, “open banking”…

These are magic, really promising words for me. But then I read: “strengthen consumer protection” (consumer?!? Ouch), “improve … access to accounts” (by whom?), “The financial data of half of the Italian population are now managed by Tink: Open banking is data sharing among the various players in the banking ecosystem”.

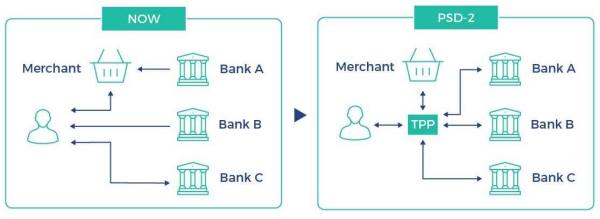

In order to understand it better, I read “What is Open Banking and PSD2?". From that piece, it seems that the purpose of Open Banking is to make it possible “to pass this rich information to third parties, who can use it to create new products (more on this later). It’s not an app or a service in its own right. It’s a way of facilitating data sharing.”

From this, I understand that this Open Banking gives third parties a standard API (Application Programming Interface) with which they can - always with my consent and for my own good, of course - download all bank transactions in a standard format, and use them to profile me, in order to offer me other financial services.

Meanwhile, poor “consumers”…

Meanwhile I - who of course am an idiot who wouldn’t know what to do with an API - am still forced to:

- endure the current madness of entering passwords and second level codes, in order to just

- download a mere PDF printout of all the transactions of the current quarter or, in the best cases, a list in Excel or CVS format for the last 12 months, not ten years

- with a different procedure, and data formatting, for every bank I have accounts with

Dear EU, if you wanted to offend me you succeeded: but please understand that your citizens may be ignorant, but not really dumb.

Dear EU, what about MY access?

Dear EU, I have been asking myself for at least 5 years why, with all this proliferation of APIs left, right and center, I still cannot automatically download, maybe once a week, all my bank and card data (debit, credit, etc.), and import them either in some personal finance manager or business accounting software of my own choice. Including Free/Open Source Software that everybody could freely modify to offfer services to individuals or businesses, of course.

But no, only third parties can automatically download those data, not me: do you think this is a serious, respectful way to treat your citizens? Please EU, tell me I got it wrong, and that all this Open Banking/PSD stuff means that my bank will be obliged Real Soon Now to give access to those APIs to me too!

Dear EU, let’s not repeat the same old mistakes

Dear EU, I understand your embarrassment for not doing anything about the SWIFT scandal of 2006 until 2013, when after Snowden you could not pretend anymore that nothing was happening, or keep ignoring the advice that your experts had given to you almost twenty years ago. But…

Dear EU, please stop kidding me and acknowledge that, rather than countering certain filth (do we agree that they are filthy?), you desperately yearn to create your own versions of Echelon, NSA and Five Eyes, to massively collect data on every activity of your citizens, and give a competitive advantage to some of our local elites, to create EU versions of Google, Amazon and Facebook, as the Chinese have already done and Russia is probably doing.

Dear EU: is this really how you want to grow? Must you really use these methodsto “stay in business”? Because if that were the case then I have bad news for you: you’ve already lost.

There ARE alternatives

Dear EU, don’t pretend to ignore that there are (since 1989) system for anonymous digital payments, including Free as in Freedom implementations that could be tested tomorrow.

Dear EU, please amaze me; show me that you are going play a leading role in the construction of the future digital civilization: place yourself at the head of the new digital humanism that is being born.

This is what matters, not consumers, “dashboards”, competition and other banalities.

Image source: PSD2 - A New Banking Era

Who writes this, why, and how to help

I am Marco Fioretti, tech writer and aspiring polymath doing human-digital research and popularization.

I do it because YOUR civil rights and the quality of YOUR life depend every year more on how software is used AROUND you.

To this end, I have already shared more than a million words on this blog, without any paywall or user tracking, and am sharing the next million through a newsletter, also without any paywall.

The more direct support I get, the more I can continue to inform for free parents, teachers, decision makers, and everybody else who should know more stuff like this. You can support me with paid subscriptions to my newsletter, donations via PayPal (mfioretti@nexaima.net) or LiberaPay, or in any of the other ways listed here.THANKS for your support!